Tax Avoidance In Malaysia

Pdf Cash Economy Tax Evasion Amongst Smes In Malaysia

Pdf Government Ownership And Corporate Tax Avoidance Empirical Evidence From Malaysia

Pdf Issues Challenges And Problems With Tax Evasion The Institutional Factors Approach

Pdf Government Ownership And Corporate Tax Avoidance Empirical Evidence From Malaysia Semantic Scholar

Is Tax Avoidance Legal In Malaysia

Chapter 1

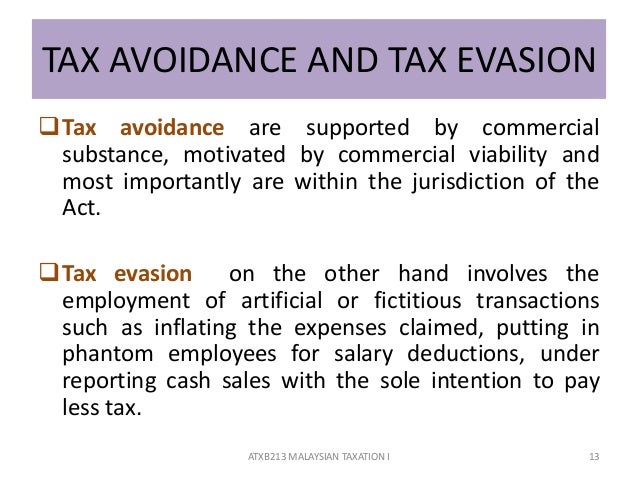

In malaysia income tax act contains general and specific anti avoidance provision which empowers the director general to disregard schemes that are not commercially justified or are merely set up to avoid tax despite their legal form.

Tax avoidance in malaysia. From the perspective of revenue authorities it is equally important to counter tax avoidance. Malaysia s progressive personal income tax system involves the tax rate increasing as an individual s income increases starting at 0 for up to rm5 000 earned to a maximum of 28 for annual income of over. It discusses the decision of the court of appeal in a recent tax case and the questions on the parameter of legitimate tax planning. The text of this agreement signed on 26 december 1968 and is shown in annex a.

Pwc alert issue 116. In malaysia by virtue of s 140 1 the dgir is entitled to disregard or vary any transaction that is created merely for the purposes of tax avoidance. If you are working in malaysia for more than 182 days a year the government considers you to be a tax resident and you will pay progressive tax rates and be eligible for tax deductions. Businesses avoid taxes by taking all legitimate deductions and tax credits and by sheltering income from taxes by setting up employee retirement plans and other means all legal and under the internal revenue code or state tax codes.

Income tax in malaysia is imposed on income accruing in or derived from malaysia resident and business. The australian position is similar to malaysia. Singapore and the government of malaysia for the avoidance of double taxation and the prevention of fiscal evasion with respect to taxes on income. Tax avoidance is the legitimate minimizing of taxes and maximize after tax income using methods included in the tax code.

If the dominant purpose of a transaction has no commercial purpose then that transaction will be disregarded or varied as being for the purpose of tax avoidance by tax authority there. Although tax avoidance is acceptable in the eyes of law in malaysia the tax authority taken an extreme change of stance since 2010 and triggered section 140 of the malaysia income tax act more often that it does historically. Thus in most tax jurisdictions anti avoidance provisions are included in the tax laws to defeat or pre empt anticipated avoidance schemes mischief or to plug loopholes that have come to light. One thing worth mentioning is malaysia has an extensive number of double tax treaties available for the avoidance of double taxation.

However this particular section is far from perfect to deal with tax avoidance issue. Section 140 of the act is indeed an anchor provision concerning tax avoidance.

Tax Avoidance Evasion And Planning In Malaysia Malaysia Taxation

Pdf Measures Of Corporate Tax Avoidance Empirical Evidence From An Emerging Economy

Wkisea Treading The Fine Line Between Tax Planning And Tax Avoidance

Tax Avoidance And Tax Evasion In 14 Itc Countries Ppt Download

Http Www Accaglobal Com Content Dam Acca Global Pdf Sa Nov11 Antiavoidancemys Pdf

Pdf Estimating Factors Affecting Tax Evasion In Malaysia A Neural Network Method Analysis Semantic Scholar

Ktps Consulting Tax Avoidance Case Free Loans Facebook

Penalty For Late Submission Of Personal Tax Return In Malaysia

Pdf The Influence Of Education On Tax Avoidance And Tax Evasion

/tax-avoidance-vs-evasion-397671-v3-5b71dfc846e0fb0025e54177.png)

Tax Avoidance And Tax Evasion What Is The Difference

Https Heinonline Org Hol Cgi Bin Get Pdf Cgi Handle Hein Journals Intaxjo21 Section 14

Http Www Ukm My Fep Perkem Pdf Perkemvii Pkem2012 5d4 Pdf

Pdf The Relationship Of Corporate Tax Avoidance Cost Of Debt And Institutional Ownership Evidence From Malaysia Semantic Scholar